News broke this morning that Huawei CFO Meng Wanzhou had been arrested in Canada, and the first reaction was shock. This kind of move goes beyond ordinary commercial competition. Major powers compete all the time, but openly breaking economic and political norms is another matter. When rules are discarded, everyone pays more: transaction costs rise, uncertainty spreads, and the risk of failed deals increases for every participant.

What is also striking is that the arrest happened on December 1, yet it only surfaced in the news five full days later. That delay says a lot about how limited and slow some information channels can be.

Meng Wanzhou’s arrest was widely understood in the context of U.S. pressure on Huawei’s telecom business. The more immediate question is practical rather than symbolic: if Washington tightens export controls on components, how exposed is Huawei to American suppliers, and how easily could those parts be replaced?

Looking at Huawei’s supplier structure, the answer is uncomfortable. Even if alternatives exist in theory, the company’s core upstream network is concentrated in the United States, Europe, Japan, and South Korea. And the problem is not only the United States itself. In strategic technology sectors, U.S. export restrictions often do not stop at American borders. European countries, Japan, and South Korea may follow the same line, especially on chips and other key inputs.

That means the issue is bigger than one company. If a Chinese technology firm is comprehensively blocked by the United States and its allies, survival becomes much harder than many people assume. It also underlines a long-standing structural weakness: China cannot rely indefinitely on growth driven by infrastructure and real estate while remaining vulnerable in high-end technology. Once export controls target critical components, the lack of domestic alternatives becomes painfully clear.

A supply chain with more than 2,000 vendors

According to a statistical review by analysts Cheng Cheng and Li Yajun at Guosen Securities, Huawei has accumulated more than 2,000 suppliers.

From the upstream category perspective, the companies that had remained Huawei “gold suppliers” for ten consecutive years included DHL, Foxconn, Qualcomm, and Analog Devices. Two of those are chip-related suppliers, while the other two provide assembly and logistics services.

Among suppliers serving Huawei’s consumer products such as phones and PCs, there were 28 major companies. More than 30% of them were chip suppliers, led by firms such as Qualcomm, Broadcom, and Intel. Within that group, CPU suppliers alone accounted for more than half.

The second major category consisted of optoelectronic components used in production equipment, with established names such as Texas Instruments, Murata, and Analog among the major suppliers.

Huawei has its own chip arm, but still depends heavily on imports

Huawei’s upstream demand profile shows both strength and limitation.

Its wholly owned chip subsidiary, HiSilicon, had developed 200 chips with independent intellectual property rights and had filed 5,000 patents. That is significant, and it means Huawei’s level of in-house development is relatively high compared with many hardware companies.

But self-development is not the same as self-sufficiency. Huawei still imported large volumes of chips, and even HiSilicon’s Kirin processors were based on ARM’s licensed architecture.

That detail matters. Owning designs is helpful, but if the underlying architecture, software tools, manufacturing ecosystem, or key supporting components remain external, the supply chain is still exposed.

Huawei was already one of the world’s biggest chip buyers

A Gartner report said Huawei was the world’s fifth-largest semiconductor buyer in 2017, with total chip purchases of about $14 billion, up 32.1% year over year.

A separate report from CCID Think Tank, an institute under China’s Ministry of Industry and Information Technology, showed that Huawei’s chip procurement total was already around $14 billion in 2015. That spending included roughly:

- $1.8 billion in Qualcomm chips

- $680 million in Intel chips

- $580 million in Micron chips

- $600 million in Broadcom chips

- $560 million in Xilinx chips

- $540 million in Cypress/Spansion chips

- $450 million each in Skyworks and Qorvo chips

- nearly $400 million in Texas Instruments chips

These numbers make the dependency much easier to see. Huawei was not buying small supplementary volumes from a few U.S. firms. It was deeply embedded in a global semiconductor supply system dominated by American and allied companies.

What Huawei’s 50 core suppliers reveal

A review of Huawei’s 50 core suppliers shows that the supply chain for PCs, phones, tablets, and other personal products spans nearly every layer of modern electronics.

Upstream vendors covered:

- sensors used in data collection and communications

- RF connectors and antenna-related components

- chip design and critical chips for data processing

- storage, including NAND flash, memory, and hard drives

- software used in end-user interaction and system support

Rather than relying on one source in each category, Huawei typically used multiple suppliers. Companies involved across these areas included ARM, Qualcomm, Broadcom, NXP, and AAC Technologies.

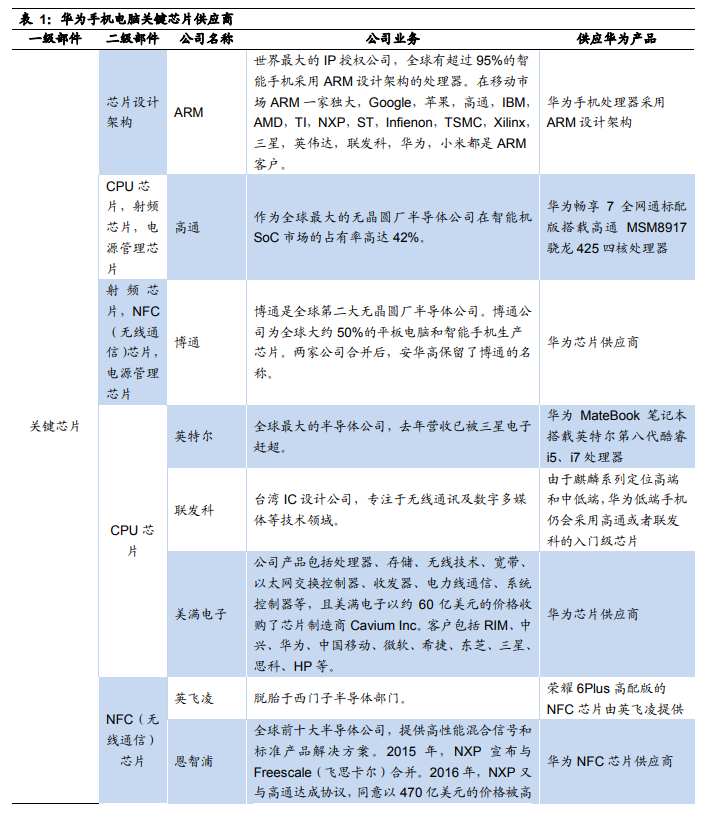

1) Chip suppliers

For chip design architecture, ARM was the main provider.

Qualcomm and Broadcom supplied Huawei with a near full range of chip categories. CPU-related suppliers included Intel, MediaTek, and Marvell. NFC suppliers included Infineon and NXP. Power-management chips mainly came from Analog Devices.

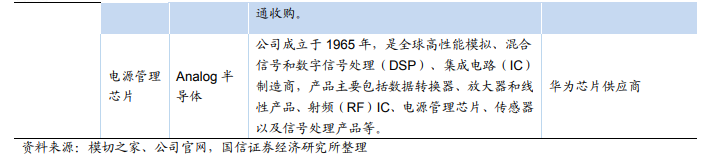

2) RF and connector suppliers

Huawei’s RF connector ecosystem was split across several specialist vendors.

RF antenna suppliers included Huber+Suhner, Qorvo, and Rosenberger. Connector suppliers included Amphenol, Hirose, and Zhongli Electronics.

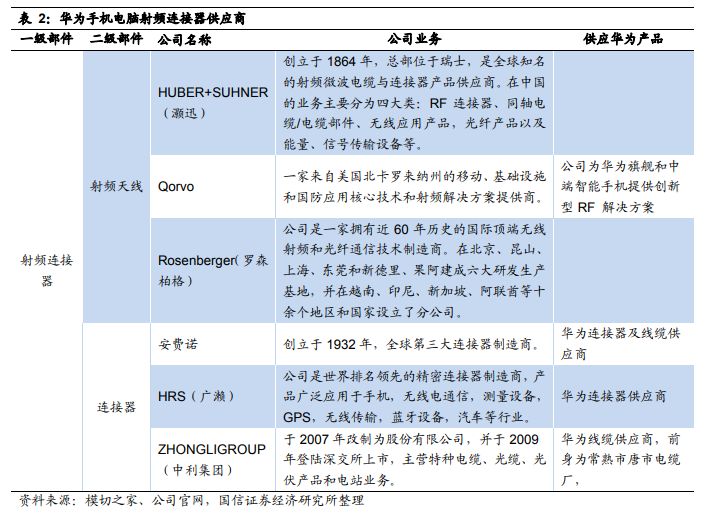

3) Storage suppliers

On storage, the picture was similarly international.

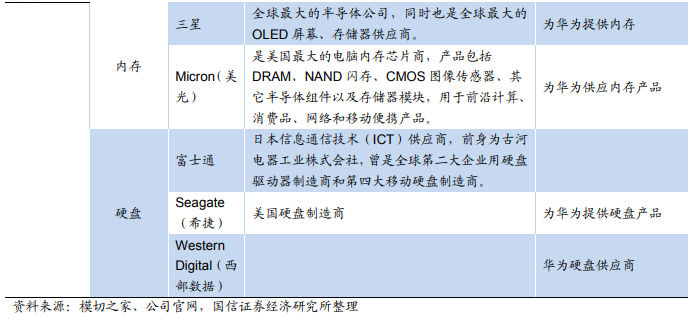

Flash suppliers included SK Hynix and Toshiba. Memory suppliers included Samsung and Micron. Hard-drive suppliers included Fujitsu, Seagate, and Western Digital.

4) Sensor and interface suppliers

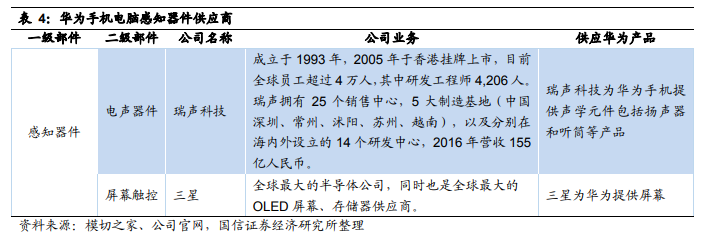

Key sensor-related suppliers included AAC Technologies for acoustic components and Samsung for display touch solutions.

5) Power, software, and other support vendors

Other suppliers covered areas that are less visible to consumers but essential to operations.

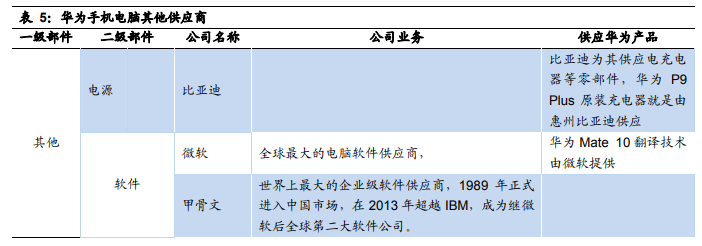

These included BYD for power-related supply, and software providers such as Microsoft, Oracle, and Synopsys.

Domestic strength existed, but mostly at the lower layers

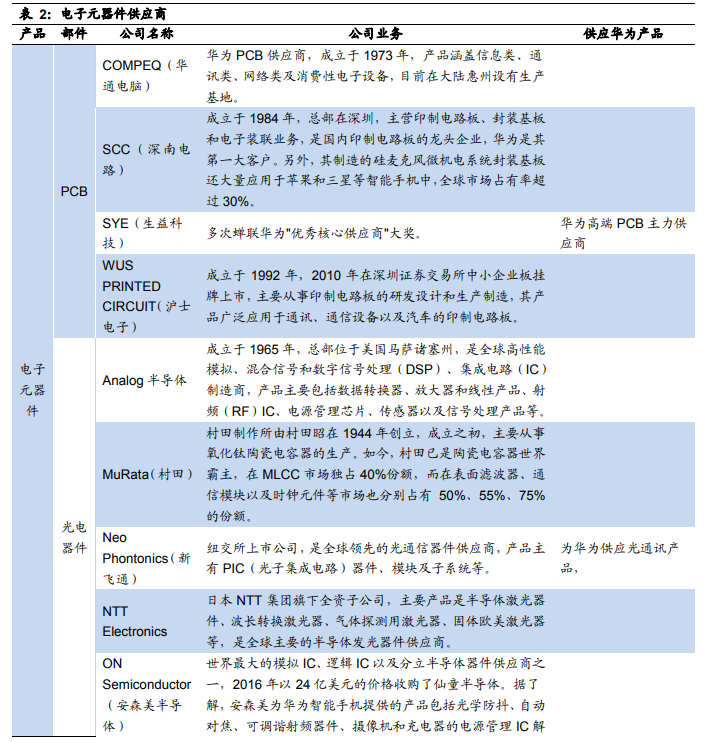

Looking at the whole upstream system, Huawei’s electronic component sourcing ran from basic printed circuit boards all the way to parts used for circuit logic design.

The strongest domestic presence was in PCB manufacturing. Core suppliers in that area were mainly Chinese companies, including Shengyi Technology, Shennan Circuits, and WUS Printed Circuit.

But once the supply chain moved into higher-value electronic components, especially the parts that determine performance and functionality, the dependence shifted outward. Many of those products came mainly from American and Japanese companies, including Murata and Texas Instruments.

That divide is crucial. Basic manufacturing capability matters, but it does not erase dependence on foreign companies for the most advanced or irreplaceable parts.

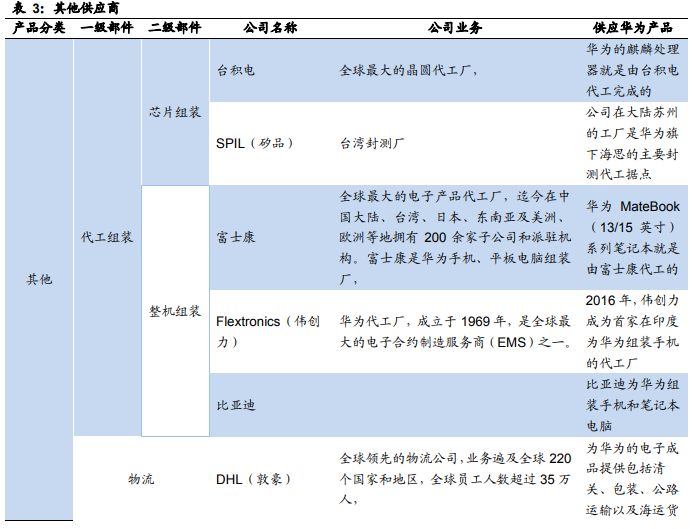

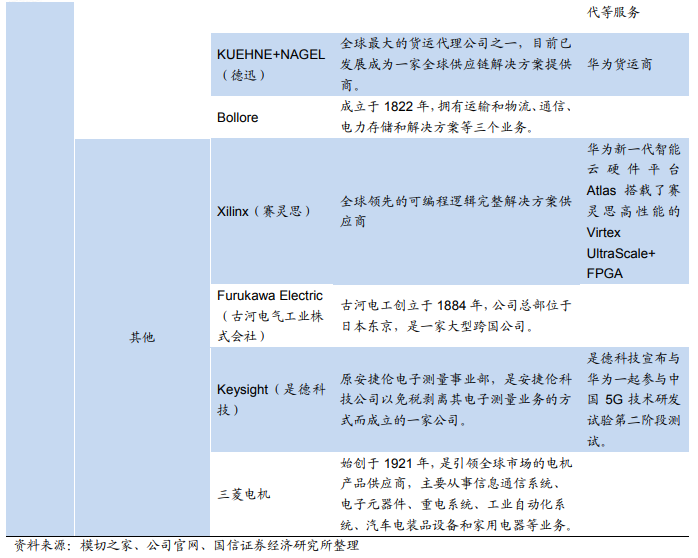

Assembly and logistics were more diversified

Outside the component layer, other suppliers mainly provided product assembly and transportation services.

Contract manufacturing was dominated by Chinese-linked companies, with Taiwanese firms playing a central role. TSMC and Foxconn were among the key names. Logistics providers were selected from a more international pool. Huawei also relied on a number of broader service providers.

The immediate market reaction to Meng Wanzhou’s arrest

Earlier that day, multiple media outlets reported that Meng Wanzhou had been detained in Canada. Meng is the daughter of Huawei founder Ren Zhengfei. After the news spread, U.S. stock-index futures fell sharply, and Dow futures were at one point down 500 points.

Huawei later responded publicly, saying it was not aware of any wrongdoing by Meng Wanzhou and that it believed the legal systems of Canada and the United States would ultimately reach a fair conclusion.

Huawei’s 2018 gold suppliers

Huawei’s 2018 gold supplier list included a broad mix of chipmakers, materials companies, optics firms, software vendors, logistics providers, and manufacturers:

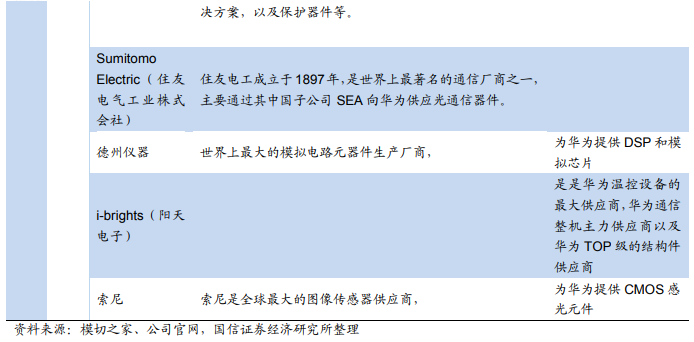

Huber+Suhner, Xilinx, Marvell, Foxconn, Shengyi Electronics, Zhongli Group, Fujitsu, WUS Electronics, Micron, Hirose, BYD, Murata, Sony, Largan Precision, Qualcomm, Analog Devices, CommScope, Amphenol, Luxshare Precision, Unimicron, Molex, Nexans, BOE, Yangtian Electronics, AVIC Optoelectronics, Oracle, Sumitomo Electric, ON Semiconductor, COSCO Shipping Group, SF Express, Sinotrans, Amperex Technology Limited, Sunny Optical, Tianma, SK Hynix, Rohde & Schwarz, Keysight Technologies, AIG, Spirent, Red Hat, SUSE, TXC Corporation, Toshiba Memory, Seagate, Western Digital, Accelink, Xinda Technology, Synopsys, HGTECH, YOFC, STMicroelectronics, Skyworks, Microsoft, Shennan Circuits, NeoPhotonics, Qorvo, Furukawa Electric, AAC Technologies, Lian En Electronics, Sumicem, Goertek, Compeq, Mitsubishi Electric, Samsung, and Nanya Technology.

Taken together, the list makes one point unmistakable: Huawei had built an enormous and sophisticated supply chain, but the highest-value links in that chain were still concentrated outside China. In a normal global market, that is a sign of integration. Under export controls, it becomes a strategic vulnerability.